Understanding the duration and impact of a hard credit pull is crucial for maintaining financial health. Whether you're applying for a loan, credit card, or mortgage, a hard inquiry can significantly affect your credit score. But how long does it last? And more importantly, how can you mitigate its effects? In this comprehensive guide, we will delve into the details of hard credit pulls and provide actionable insights to help you manage your credit responsibly.

Millions of consumers worldwide undergo hard credit pulls each year, often without fully grasping their implications. These inquiries are a necessary part of the credit evaluation process, but they can have lasting effects on your credit report. By understanding how long a hard credit pull lasts and its potential impact, you can make more informed financial decisions.

This article will provide a detailed breakdown of hard credit pulls, including their duration, effects on credit scores, and strategies to minimize their impact. Whether you're a first-time borrower or an experienced credit user, this guide will equip you with the knowledge you need to maintain a strong credit profile.

Read also:Bolly4ucom Your Ultimate Destination For Bollywood Movies And Entertainment

Table of Contents

- What Is a Hard Credit Pull?

- How Long Does a Hard Credit Pull Last?

- Hard Pull vs. Soft Pull

- Impact of a Hard Credit Pull on Your Credit Score

- Factors Affecting Credit Score After a Hard Pull

- Recovery Time for Your Credit Score

- Strategies to Minimize the Impact of Hard Credit Pulls

- Common Mistakes to Avoid When Managing Hard Credit Pulls

- Alternatives to Hard Credit Pulls

- Conclusion: Take Control of Your Credit Health

What Is a Hard Credit Pull?

A hard credit pull, also known as a hard inquiry, occurs when a lender or creditor checks your credit report to evaluate your creditworthiness. This typically happens when you apply for a loan, credit card, mortgage, or other forms of credit. Unlike soft inquiries, which do not affect your credit score, hard pulls are recorded on your credit report and can have a lasting impact.

Hard inquiries are initiated with your consent and are an essential part of the credit approval process. However, they signal to lenders that you may be seeking new credit, which can increase your financial risk profile. Understanding the mechanics of a hard credit pull is the first step toward managing its effects.

Why Do Lenders Perform Hard Credit Pulls?

Lenders perform hard credit pulls to assess your credit history, payment behavior, and overall financial responsibility. This information helps them determine whether to approve your application and at what interest rate. Key factors evaluated during a hard pull include:

- Payment history

- Credit utilization ratio

- Length of credit history

- New credit accounts

- Mix of credit types

How Long Does a Hard Credit Pull Last?

A hard credit pull remains on your credit report for two years. During this period, it can influence your credit score, particularly in the first few months after the inquiry. However, its impact diminishes over time as your credit history evolves and new information is added to your report.

It's important to note that not all hard inquiries affect your credit score equally. For example, multiple inquiries for the same type of credit product, such as auto loans or mortgages, may be treated as a single inquiry if they occur within a specific time frame (typically 14-45 days). This is known as "rate shopping" and is designed to prevent penalizing consumers who are comparing offers.

Does Every Hard Pull Affect Your Credit Score?

Not necessarily. While most hard credit pulls impact your credit score, some may have minimal or no effect, depending on your overall credit profile. For instance, if you have a long credit history with a strong track record of timely payments, the impact of a single hard pull may be negligible. Conversely, if you have a thin credit file or a history of missed payments, the effect could be more pronounced.

Read also:Meet The Cast Of Christmas Vacation Movie A Festive Journey

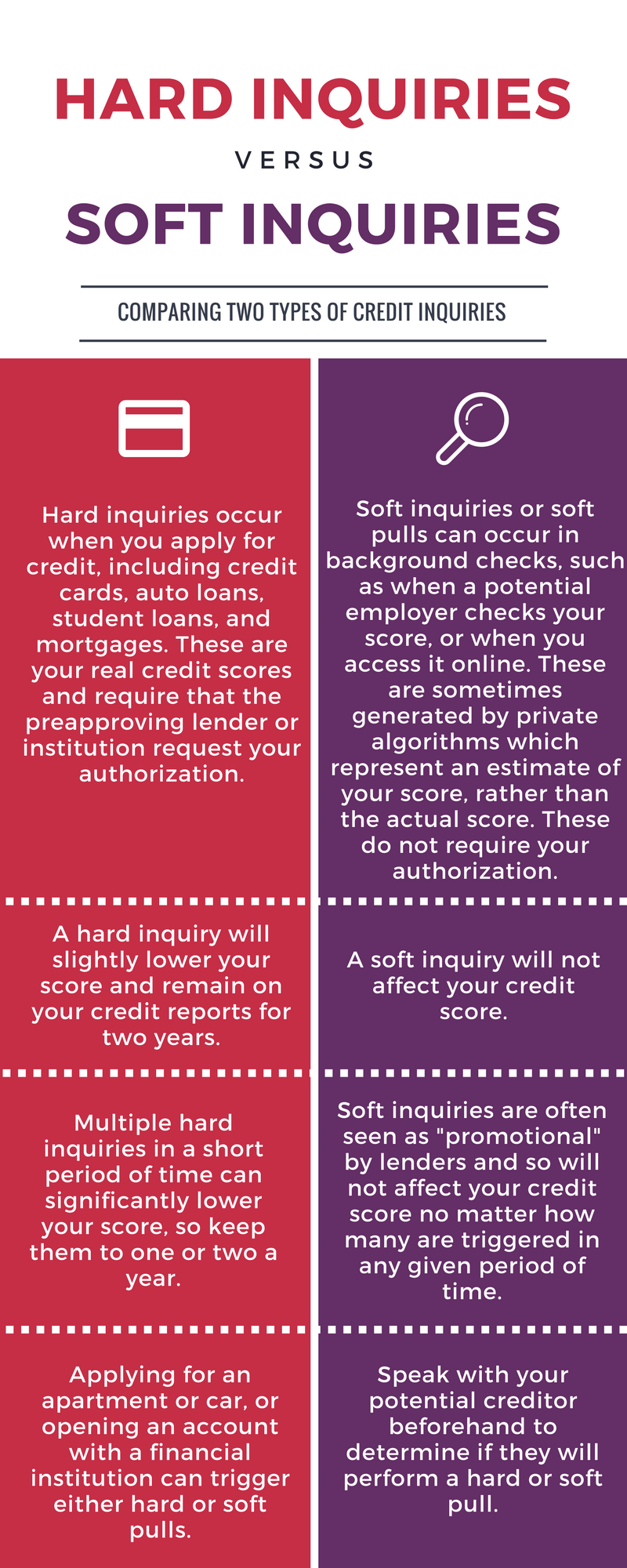

Hard Pull vs. Soft Pull

Understanding the difference between hard and soft credit pulls is essential for managing your credit health. While both types of inquiries involve accessing your credit report, they serve different purposes and have distinct implications.

Hard Pull: A hard credit pull is initiated when you apply for credit and requires your consent. It affects your credit score and remains on your report for two years.

Soft Pull: A soft credit pull occurs when you or a third party checks your credit report for informational purposes. Examples include checking your own credit score, pre-approval offers, or employment background checks. Soft inquiries do not affect your credit score and are not visible to lenders.

Key Differences Between Hard and Soft Pulls

- Purpose: Hard pulls evaluate creditworthiness, while soft pulls provide information.

- Impact: Hard pulls affect credit scores, whereas soft pulls do not.

- Visibility: Hard pulls are visible to lenders, while soft pulls are not.

Impact of a Hard Credit Pull on Your Credit Score

A hard credit pull can reduce your credit score by a few points, with the exact impact depending on your credit profile. On average, a single hard inquiry may lower your score by 5-10 points. While this may seem minor, the cumulative effect of multiple inquiries can be significant, especially if your credit history is limited.

The impact of a hard pull diminishes over time as your credit report reflects new positive activity. For most consumers, the effect is temporary and can be mitigated through responsible credit management.

How Credit Scoring Models Evaluate Hard Pulls

Credit scoring models, such as FICO and VantageScore, weigh hard inquiries as one of several factors affecting your credit score. While inquiries account for a relatively small percentage of your overall score (about 10%), they can still influence lending decisions, particularly for consumers with borderline credit profiles.

For example, if you have a high number of recent hard pulls, lenders may perceive you as a higher risk, even if your score remains within an acceptable range. This highlights the importance of limiting unnecessary credit applications.

Factors Affecting Credit Score After a Hard Pull

Several factors determine how much a hard credit pull affects your credit score. These include:

- Credit History: Consumers with longer credit histories may experience less impact from hard pulls compared to those with limited credit experience.

- Payment Behavior: A history of timely payments can offset the negative effects of a hard inquiry.

- Credit Utilization: Keeping your credit utilization ratio low demonstrates responsible credit management and can help mitigate the impact of a hard pull.

- Recent Inquiries: Multiple hard pulls in a short period can compound their effect on your credit score.

Understanding these factors can help you anticipate and manage the impact of hard credit pulls on your financial health.

Recovery Time for Your Credit Score

Recovery time for your credit score after a hard pull depends on various factors, including your credit profile and ongoing credit behavior. In most cases, the impact of a single hard inquiry fades within a few months, provided you maintain responsible credit habits.

For example, if you consistently make on-time payments, reduce your credit utilization, and avoid taking on new debt, your credit score can rebound quickly. Conversely, if you miss payments or accumulate additional debt, the recovery process may take longer.

Tips for Accelerating Credit Score Recovery

- Pay bills on time to build a positive payment history.

- Reduce credit utilization by paying down balances.

- Avoid applying for new credit unless absolutely necessary.

- Monitor your credit report regularly for errors or discrepancies.

Strategies to Minimize the Impact of Hard Credit Pulls

While hard credit pulls are unavoidable in some cases, there are strategies you can employ to minimize their impact:

- Limit Credit Applications: Only apply for credit when necessary and ensure you meet the lender's requirements.

- Pre-Qualify for Credit: Use soft pulls to pre-qualify for credit offers without affecting your score.

- Time Your Applications Strategically: If you're shopping for a loan or mortgage, complete your applications within a short time frame to benefit from rate shopping provisions.

- Monitor Your Credit Report: Regularly review your credit report to ensure accuracy and address any issues promptly.

By adopting these strategies, you can maintain a strong credit profile while managing the effects of hard credit pulls.

Common Mistakes to Avoid When Managing Hard Credit Pulls

Many consumers make mistakes that exacerbate the impact of hard credit pulls. Some common errors to avoid include:

- Applying for multiple credit accounts simultaneously without a clear plan.

- Ignoring the importance of credit utilization and payment history.

- Failing to monitor credit reports for errors or unauthorized inquiries.

- Not understanding the difference between hard and soft pulls.

Avoiding these pitfalls can help you maintain a healthy credit score and reduce the long-term effects of hard inquiries.

Alternatives to Hard Credit Pulls

In some cases, you may have alternatives to hard credit pulls that allow you to evaluate credit offers without impacting your score. These include:

- Soft Pulls: Many lenders offer pre-qualification or pre-approval options that use soft pulls to assess your creditworthiness.

- Alternative Data: Some lenders use non-traditional data, such as rental payments or utility bills, to evaluate credit risk.

- Secured Credit Cards: These cards require a security deposit and do not typically require a hard pull for approval.

Exploring these alternatives can help you access credit while minimizing the impact on your credit score.

Conclusion: Take Control of Your Credit Health

In conclusion, understanding how long a hard credit pull lasts and its impact on your credit score is essential for maintaining financial stability. By limiting unnecessary credit applications, managing your credit utilization, and adopting responsible credit habits, you can minimize the effects of hard inquiries and build a strong credit profile.

We encourage you to take action by monitoring your credit report regularly, pre-qualifying for credit offers, and educating yourself about credit management best practices. Share this article with others who may benefit from the insights provided, and consider exploring additional resources to further enhance your financial literacy.

Have questions or feedback? Leave a comment below, and let us know how we can assist you further in your credit journey.